The Federal Reserve’s first rate cut of 2025 marked the beginning of a new phase in cash management. Customers spent 18 months chasing 5% yields in money market funds (MMFs) only to find that advantage now fading. For trust companies and other institutions, it’s a balancing act of providing customers with competitive rates and other benefits. Customers may inquire about why their “safe cash” yields from MMFs are declining, while examiners continue to scrutinize how trust companies and financial institutions manage their uninsured exposures.

Customers Expect More Than Yield

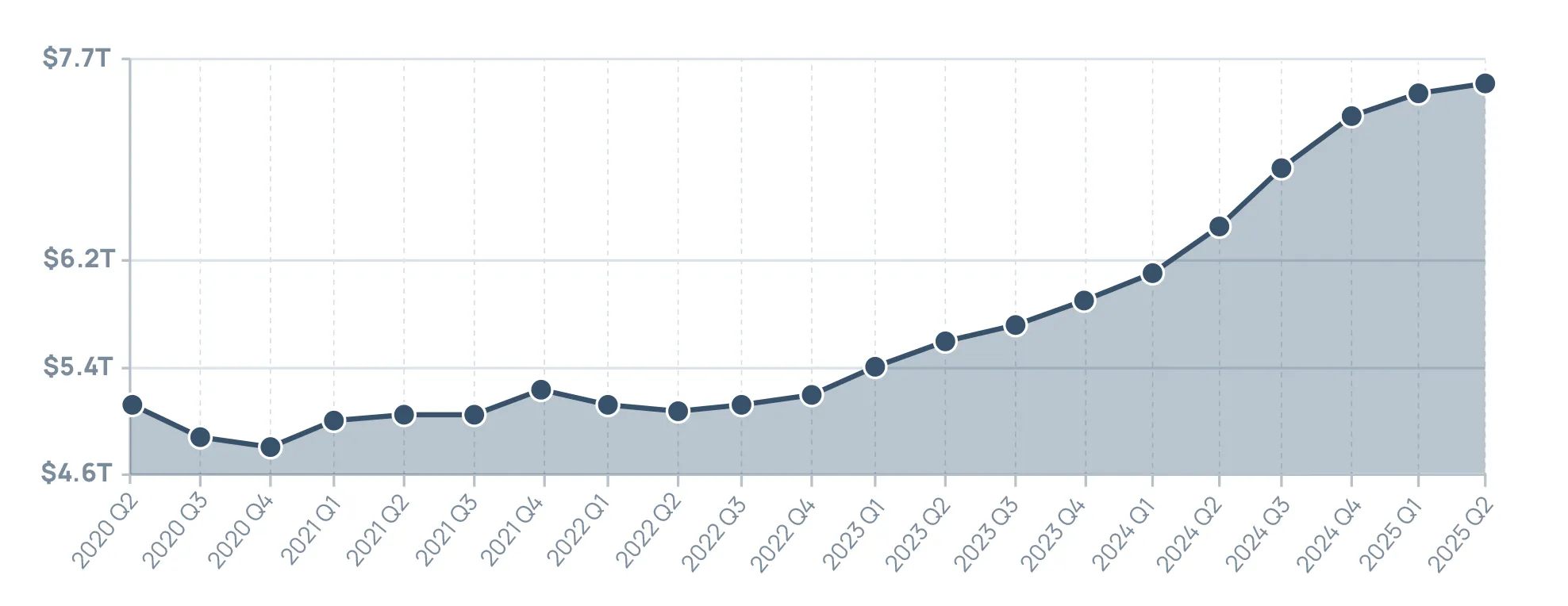

Money market funds soared to a record $7.4 trillion in September 2025, according to the Investment Company Institute (ICI) data.

The draw was simple: while FDIC national data showed savings deposit rates averaging just 0.47% in 2023 (FDIC National Rates), prime MMFs were paying north of 5% (Morgan Stanley analysis).

However, their appeal is fading fast. While UBS’ CIO has called it “an imperative to put cash to work,” (Family Wealth Report), Morgan Stanley warns that “higher money market fund returns won’t last.” (Morgan Stanley Wealth Management).

The reality: without an insured, liquid option to present, trust companies and other institutions risk eroding their customers’ trust or losing balances altogether.

Insured sweep solutions consistently meet these expectations across cycles, while avoiding the reinvestment risk commonly associated with MMFs.

Examiner Pressure on Uninsured Balances

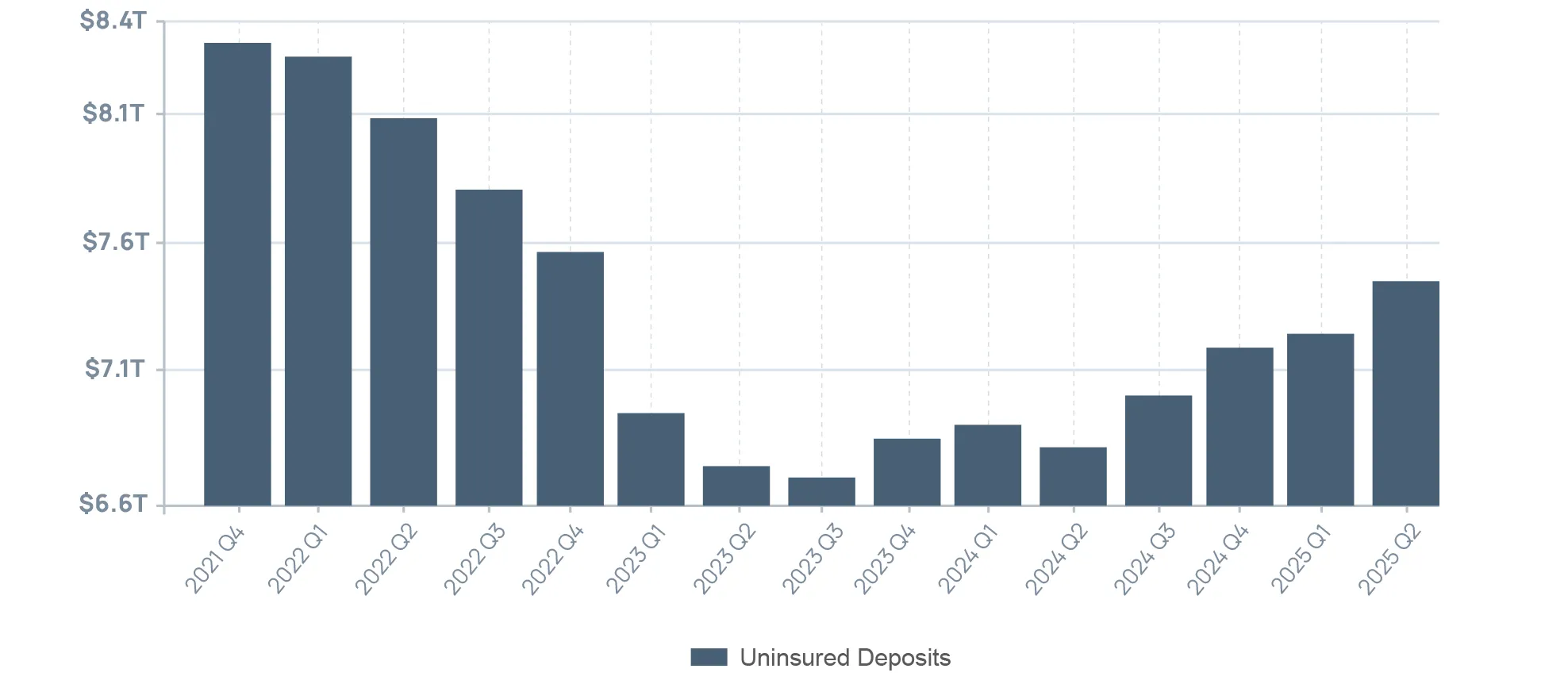

The FDIC’s Q2 2025 Quarterly Banking Profile reported a $218.5 billion (3.0%) increase in uninsured deposits. Examiners expect not just awareness but clear action. Through reciprocal deposit programs, trust companies and other institutions can provide their customers with access to expanded deposit insurance coverage through a network of FDIC-insured receiving banks. This structure diversifies exposure for customers and demonstrates a proactive approach to reducing uninsured balances, which has drawn regulatory scrutiny in recent years.

Importantly, under S.2155 (the Economic Growth, Regulatory Relief, and Consumer Protection Act), qualifying reciprocal deposits receive favorable regulatory treatment as non-brokered deposits up to the lesser of $5 billion or 20% of liabilities (FDIC guidance).

Money Market Fund Uncertainty

History shows why trust companies can’t rely on MMFs as a core strategy:

Each cycle proves the same point: money market funds are cyclical, not structural. Trust companies and institutions require a solution for their customers that maintains safety and liquidity throughout the entire cycle, not just during yield spikes.

Redefining the Standard

The measure of leadership may be shifting away from who captured yesterday’s 5% return to who best safeguards their customers’ confidence.

Insured sweep and reciprocal deposit programs align with these pillars, resulting in firms’ cash management strategies being aligned with sound judgment and responsible oversight.

The Demand Deposit Marketplace® (DDM®) program enables trust companies to offer their customers access to expanded FDIC-deposit insurance coverage on their funds through a nationwide bank network. Bank-affiliated trust companies can count these balances toward stable wholesale funding under the reciprocal deposit exception to brokered deposits. For independent trust companies, the DDM program often simplifies operations while strengthening customer relationships.

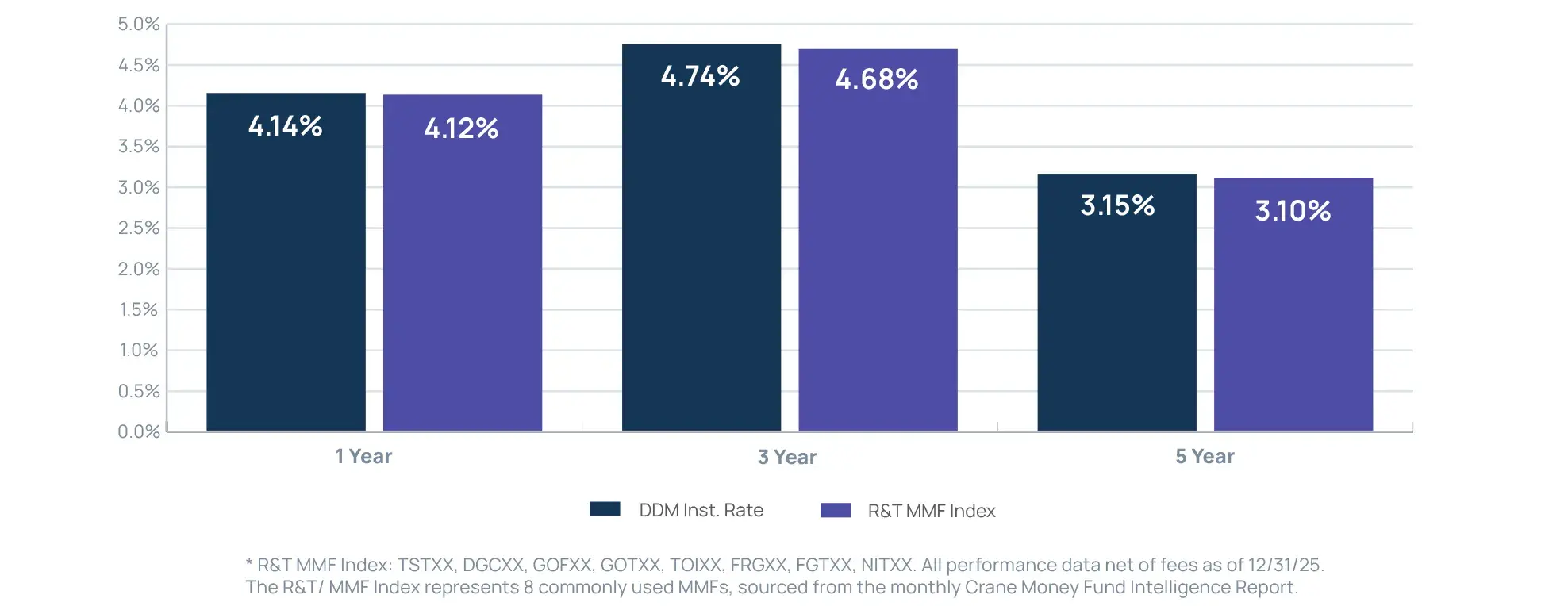

Over 1-, 3-, and 5-year periods, rates at which interest is paid under the DDM Program’s Institutional Rate have historically been higher than the yields on a basket of institutional government MMFs*. The result is higher customer satisfaction.

Performance Data

R&T’s solutions integrate with more than 50+ core processors and adapt to client formats without requiring changes to existing systems, giving trust companies the flexibility to adopt insured cash programs without disruption. R&T’s portals, APIs, and data-exchange tools also provide real-time visibility into balances, transactions, and reporting, allowing trust officers to access the information they need without manual workarounds.

The Imperative

Rate cycles will shift. Market headlines will change. But trust companies and other institutions’ responsibilities remain constant: protect principal, preserve liquidity, and inspire customer confidence.

That’s why insured sweep solutions are no longer optional and are emerging as a new standard solution. With R&T’s proven leadership and expertise, trust company executives can navigate today’s shifting environment while positioning their institutions for long-term resilience.

Learn how R&T can help you navigate insured sweep solutions with the DDM® program.

Demand Deposit Marketplace® (DDM®) Program: FAQs for Trust Companies

1 Subject to R&T’s cut-off times. Under the DDM program, funds are deposited into demand deposit accounts (DDAs) or money market deposit accounts (MMDAs) at receiving banks or share draft accounts or share accounts at receiving credit unions. While customers’ funds are held in MMDAs or share accounts, the return of customers’ funds from the DDM program may be delayed as, under federal regulations, the receiving institution is permitted to impose a delay of up to seven days on any withdrawal request from an MMDA or share account.

2 While interest rates obtained on funds placed at receiving institutions under the DDM program may, under certain circumstances, outperform cash alternatives, such as money market funds, the primary objective of the DDM program is to provide customers with convenient access to expanded FDIC insurance coverage on their funds (and not for investment enhancements or higher rates of returns or profits).