When capital preservation, liquidity, and yield are top priorities, financial institutions and wealth managers often choose between cash sweep programs and Money Market Funds (MMFs).

While both aim to preserve capital and provide access to liquidity, they differ significantly in structure, risk exposure, regulatory treatment, and operational impact.

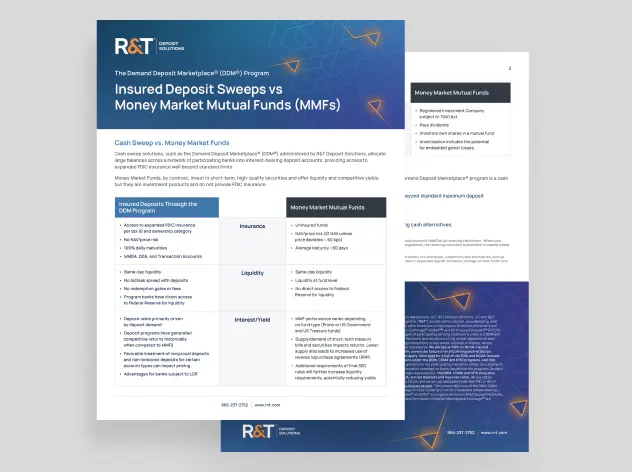

Cash Sweep vs Money Market Funds

-

Cash Sweep Solutions

Cash sweep solutions, such as the Demand Deposit Marketplace® (DDM®) program, are designed to support large accounts by allocating customer funds across a network of participating banks into interest-bearing deposit accounts. By allocating funds in this manner, customers gain access to expanded FDIC deposit insurance coverage, often far exceeding the standard maximum deposit insurance amount (currently $250,000 per customer identifier (e.g., TIN)1 per account ownership category, up to the applicable DDM Program Limit.

-

Money Market Funds

In contrast, Money Market Funds, structured as registered investment companies, are subject to the Investment Company Act of 1940 and invest in a mix of short-term, high-quality instruments such as U.S. Treasuries, commercial paper, and repurchase agreements. MMFs offer competitive returns and high liquidity, but do not provide access to FDIC insurance.

Risk and Access to Deposit Insurance Coverage

Perhaps the most significant difference between the two options relates to risk and insurance. MMFs do not provide access to FDIC deposit insurance and carry some level of market and credit risk, depending on their portfolio composition. Although structured to maintain a stable $1 net asset value (NAV), MMFs may experience price volatility under certain market conditions.

Cash sweep programs, on the other hand, while subject to interest rate risk, provide access to expanded FDIC deposit insurance by allocating deposits across multiple participating banks, which mitigates credit risk. This feature can be especially valuable during times of financial uncertainty.

The DDM Program vs Money Market Funds

Market Conditions and Liquidity

Both the DDM program and MMFs offer same-day access to funds. However, the DDM program generally offers more predictable liquidity2.

While MMFs offer daily liquidity, they may be subject to redemption gates or liquidity fees during periods of market stress, which can restrict immediate access to cash.

Regulatory Differences Between MMFs and the DDM Program

Regulatory frameworks further distinguish these solutions. Funds held within the DDM program reside within the traditional banking system and are subject to bank-specific regulations. These banking regulations are designed primarily to ensure the bank’s safety and soundness. MMFs structured as registered investment companies are regulated by the Securities and Exchange Commission and are subject to evolving regulatory reforms that are focused primarily on investor protection. In recent times, regulatory reforms enacted by the SEC have increased liquidity requirements in some cases, reducing yield potential.

Yield Considerations

Yield profiles can vary between the two. Interest rates obtained on bank deposits swept into the DDM program are generally influenced by demand for deposits and can be particularly competitive in certain rate environments3. MMF performance, by contrast, depends on the fund type—Government, Treasury, or Prime—and broader market dynamics such as Treasury supply and the Federal Reserve’s Reverse Repo Facility.

Operational Considerations

Operationally, funds within the DDM program are simply bank deposits, simplifying accounting and eliminating the need to amortize gains or losses. MMFs, as investment securities, may require more complex accounting treatment and operational oversight. For organizations aiming to streamline back-office processes, the DDM program may offer smoother integration into existing workflows.

Ultimately, choosing between the DDM program and MMFs comes down to each firm’s priorities. If top concerns are capital preservation, access to enhanced deposit insurance coverage, and operational efficiency, the DDM program may be a more suitable option.

Both products serve important roles in modern liquidity management. As regulatory frameworks evolve and interest rate dynamics shift, understanding the nuanced differences between the DDM program and MMFs is crucial.

A thoughtful evaluation of your organization’s liquidity strategy, especially in terms of access to deposit insurance, accessibility, and yield, can determine the best fit, which may include a combination of the two.

Insured Deposit Sweeps vs Money Market Mutual Funds (MMFs)